The Federal Reserve met today and decided to leave interest rates unchanged. But is this really important?

The Fed has raised interest rates multiple times in the past 18 months, but equity markets have continued moving higher and bond markets haven’t shown much volatility. More importantly than the decision on interest rates today was its statement on their balance sheet. The Fed said that they would begin “implementing its balance sheet normalization program relatively soon.”

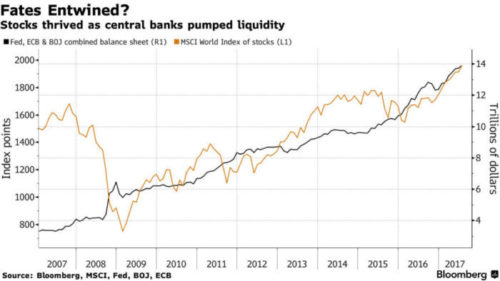

Global central banks have been printing trillions of dollars over the past 10 years. The chart below via Bloomberg shows the combined balance sheet of the US Federal Reserve, the European Central Bank and the Bank of Japan, plotted against a global index of stocks. Notice a pattern?

This is why watching the Fed is so important. However, while most people focus on interest rates, it is actually more important to focus on what central banks are doing with their balance sheets. If expanding their balance sheets has resulted in higher equity prices, it is logical to think that shrinking balance sheets could have the opposite effect.

These balance sheet have expanded by “printing” digital currency. It would be like you or me going into our bank account online and adding a couple “zeros” to the end of the number. By a couple, I mean 12. The Fed then takes these extra zeros and buys government bonds. Theoretically, the sellers of these bonds then put the cash to work in the real economy.

But what has happened is that this cash has been put to work in the stock market, resulting in increased corporate buy-backs and generally rising stock prices.

In Fed-speak, “normalization” means “smaller”. This could be accomplished in a few different ways:

- As bonds mature, don’t repurchase new bonds. In other words, remove a couple zeros.

- Sell existing bonds back into the open market. Sell a couple of those zeros.

- Create inflation that reduces the relative size of the current bonds compared to future purchasing power.

The key question is “if normalization begins, what happens next?” I wish we knew the answer to that question. In my opinion, central banks don’t know the answer to that question either. The Fed provides their version of Policy Normalization here: https://www.federalreserve.gov/monetarypolicy/policy-normalization.htm

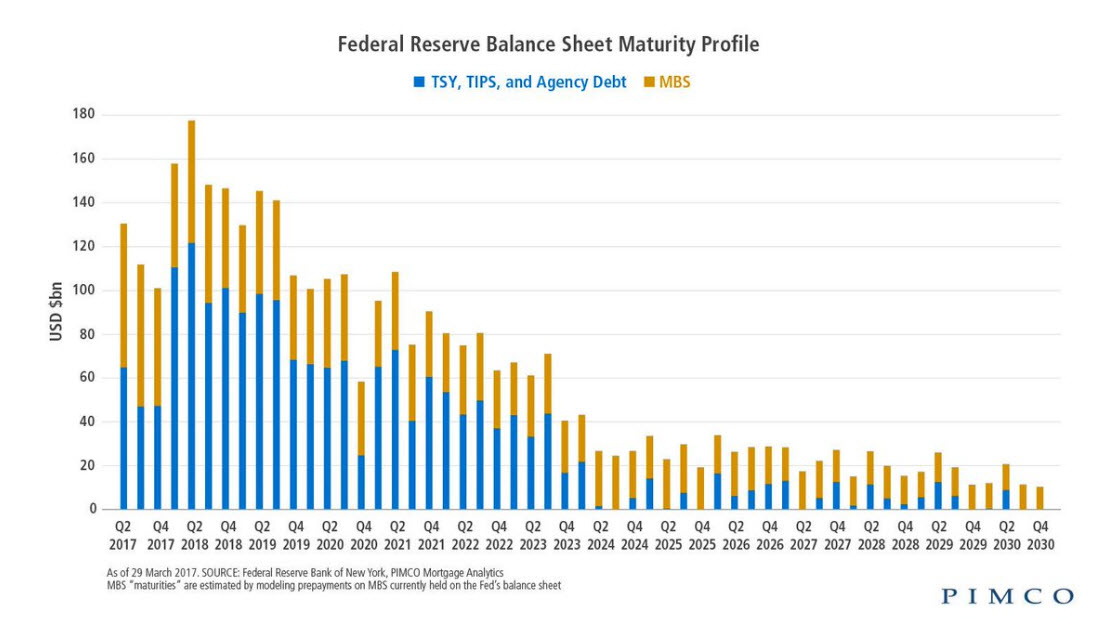

However, we can look at the maturity schedule of the balance sheet to see how much this normalization means in dollar terms. The chart below from PIMCO shows this maturity schedule. I see risks of normalization in the large increase of maturing assets in Q1 and Q2 of 2018. This could be the “tell” for future market volatility, since the Fed has not begun to actually normalize yet.

So what are we supposed to do?

- Identify outcomes. The fed has pushed stocks further than many people thought, and could continue to push them even higher for longer if normalization is gradual. On the other hand, normalization could result in increased volatility and elevated downside risk.

- Know your exit. Don’t blindly hold assets without a defined exit strategy.

- Be prepared for market volatility. Both financially and emotionally. If volatility occurs, you and your portfolio will be prepared for it. If it doesn’t, enjoy the tranquility.

In the meantime, pay attention to what the Fed does with those zeros.

[/cherry_col]

[/cherry_row]