In this episode, we discuss the recent surge in COVID due to the Delta variant, compare this surge to the UK on when we may expect cases to begin to drop, look how previous surges in cases have effected both the S&P 500 and bonds, and compare different assets to get a sense of where the market may go from here.

Be a Mercenary: 3 Ways to Improve Your Investment Process

When investing, listening to common wisdom can be very productive. But not all “wisdom” is worth listening to.

Here are three philosophies that can help you improve your investment results.

1. You Don’t Have to Own Stocks Forever

There is a lot of potential risk in markets right now.

But guess what? There always is.

We’ve been trained to think that if you buy stocks, you must own them forever or else you’re doing it wrong.

Don’t buy into that kind of thinking.

It’s okay to get out. It’s okay to have stop losses. It’s okay to allocate capital to stocks right now, as long as you have the proper risk management strategies in place. In our opinion, that means having rules to move out of stocks and back into cash.

In fact, we think that you should intentionally be thinking shorter-term when it comes to stocks right now. There are signs that the stove could get hot. But avoiding it means you may be passing up on solid investment returns in the meantime.

2. Separate your Emotions from your Actions

We believe in having rules. This allows you to not have a vested emotional interest in the outcome of the stock market.

When humans predict something will happen, they create both a confirmation bias to that prediction as well as an anchoring bias to the predicted outcome.

A confirmation bias is when we look for things that support our way of thinking. Politics and social media are the ultimate examples of confirmation bias today. People like to watch and read things that support their view.

Anchoring bias refers to how we view an array of information based on an initial assumption or data point. If we view the market as one that should be rising, we tend to subconsciously view that as the primary outcome we should expect. And we don’t only actively seek out confirmation of our theory, we interpret data points and events to be supportive of that belief, whether that is the accurate way to interpret it or not.

Both of these biases result in viewing markets without the objectivity and discipline needed to be successful investors.

3. Be a Mercenary

This means you want to fight for the side that both pays you the most money and avoids the most harm.

Tech is doing well? Great. Invest there.

Inflation is coming? Great. Invest in areas that are showing benefits to that inflation.

Markets are crashing? Great. Have more cash.

Bottom line: Don’t be dogmatic. Don’t be a permabull or permabear. Try to fight for the winning side. You won’t always be right, but you’ll be on the right side of the big trends when they happen.

Having a process will help tremendously when markets get confusing. Remembering these three

Retirement Plan Choices for Small Businesses

As a small-business owner, figuring out retirement choices can be a little intimidating. How do you pick the most appropriate retirement plan for your business as well as your employees?

There are a number of choices when creating retirement plan strategies for you and your employees.

Here, we will review three of the most popular for small businesses: SIMPLE-IRAs, SEP-IRAs, and 401(k)s.

This article is for informational purposes only and is not a replacement for real-life advice, so make sure to consult your tax, legal, and accounting professionals before implementing or modifying a retirement plan.

SIMPLE-IRAs

SIMPLE stands for Savings Incentive Match Plan for Employees. This is a traditional IRA that is set up for employees and allows both employees and employers to contribute.

If you’re an employer of a small business who needs to get started with a retirement plan, a SIMPLE-IRA may be for you. SIMPLE-IRA’s provide some degree of flexibility in that employers can choose to either offer a matching contribution to their employee’s retirement account or make nonelective contributions.

In addition, employees can choose to make salary reduction contributions to their own retirement account. Some small business owners opt for a SIMPLE-IRA because they find the maintenance costs are lower compared with other plans.1,2

Distributions from SIMPLE-IRAs are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 72, you must begin taking required minimum distributions.

For a business to use a SIMPLE-IRA, it typically must have fewer than 100 employees and cannot have any other retirement plans in place.1

SEP-IRAs

SEP plans (also known as SEP-IRAs) are Simplified Employee Pension plans. Any business of any size can set up one of these types of retirement plans, including a self-employed business owner.

Like the SIMPLE-IRA, this type of retirement plan may be an attractive choice for a business owner because a SEP-IRA does not have the start-up and operating costs of a conventional retirement plan.

This is a type of retirement plan that is solely sponsored by the employer, and you must contribute the same percentage to each eligible employee. Employees are not able to add their own contributions.

Unlike other types of retirement plans, contributions from the employer can be flexible from year to year, which can help businesses that have fluctuations in their cash flow.3

Much like SIMPLE-IRAs, SEP-IRAs are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 72, you must begin taking required minimum distributions.

401(k)s

401(k) plans are funded by employee contributions, and in some cases, with employer contributions as well. In most circumstances, you must begin taking required minimum distributions from your 401(k) or other defined contribution plan in the year you turn 72. Withdrawals are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty.1

1. IRS.gov, March 4, 2021

2. Investopedia.com, April 25, 2021

3. Investopedia.com, February 23, 2021

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG, LLC, is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2021 FMG Suite.

How to Treat Your Career Like a Sport

When thinking about your business or career, it might seem odd to make comparisons to a sport. But when you zoom out and look at the similarities, they’re more closely related than you may think.

For example, a common problem many people face as they end their careers and enter retirement is a loss of purpose and a feeling of emptiness. The thing that consumed eight hours a day for the past 40 years is now gone.

Athletes face these same struggles. But they tend to face it much sooner in life. However, some athletes find themselves thriving in life after sports. Those that succeed learned many valuable lessons and picked up traits from their sport that can translate into other areas of life.

Derek Jeter, former Yankees shortstop and first-ballot Hall of Famer, is now CEO and part-owner of the Miami Marlins and co-founded the media company, The Players’ Tribune. Hall of Fame defensive end Michael Strahan took his talents and football knowledge to live TV and has co-hosted Fox NFL Sunday, $100,000 Pyramid, and even Good Morning America.

While your career may not lead to headlines and TV gigs, there are a few ways that you can treat your career like a sport to set yourself up for long-term success.

The 10,000 Hour Rule

In his book, The Outliers, Malcolm Gladwell claims that it takes roughly 10,000 hours of work to master a skill. While the specific number of hours has been challenged by many, the principle will always make sense: to be great at something, you must put in the work.

Athletes dedicate years, sometimes decades, to their craft to be the best that they can be. We shouldn’t treat our own careers much differently.

Over the course of your working career, you’re most likely going to put 10,000 hours of work in by just showing up. However, if you’re intentional about the work that’s being put in, you can begin to propel your business to heights you never imagined possible.

For example, you may want to pursue a graduate degree or additional certifications that allows you to move up in the ranks of your profession more quickly.

Possibly more importantly, putting in the work of connecting with like-minded people on the same path as you might pay major dividends. Growing an alternative skillset could lead to a career change that provides higher potential income and happiness.

When you put in the work, it’s hard not to make progress.

Be Prepared for Uncertainty

Just like athletes devote time to be mentally and physically prepared for competition, an effective way to level up in your career is by being prepared. Whether you’re interviewing for a new job or giving a presentation to your team, preparation is critical and impacts how you perform the given task.

When you’re prepared, you’re more confident. The stress that comes with uncertainty disappears when you’ve prepared appropriately, and with that, the likelihood of achieving the desired result is increased.

Be Accountable in Your Work

Being accountable is a trait that impacts many areas of life, even outside of your career. When things don’t go right, it’s easy to blame other people or external factors.

However, by taking ownership of your work, you’ll stand out from other workers, and you begin to build trust with the people around you.

While being accountable to others is excellent, it doesn’t stop there. It’s also important to be responsible for yourself and your goals.

For example, if you want to get promoted over the next year and you’ve laid out the steps needed to make it happen, stick to them. Too often, we set goals for ourselves, like New Year’s Resolutions, and end up leaving them behind when life gets in the way.

Embrace Your Team

In both the workplace and sports, being successful almost always requires good teamwork.

The backbone of a championship team usually consists of two essential factors: cohesion and communication.

But one doesn’t come without the other.

Cohesion is formed through effective and consistent communication. These two traits then begin to form a solid foundation of trust, leading to better, more efficient work.

Having a good relationship with a team or coworkers can create healthy competition, and a great example of this is the sales profession.

Imagine being a salesperson who works alone, didn’t have a team to fall back on, and didn’t know how the rest of the team was performing. They might get discouraged or lose sight of the end goal. So, there’s a reason that most sales teams operate together – it can create a healthy competitive atmosphere, increases engagement, and keeps everybody’s motives and goals aligned.

Aside from the performance aspect, embracing your team and having an enjoyable workplace makes work that much easier, and the foundation is built through being reliable, offering help to others, and being a good teammate.

The Takeaway

In our careers, it’s easy to lose sight of an end goal and feel like we’re not making progress.

But when you treat your career like a sport and strive to get better, it starts to feel like a natural part of your life, not just another task to check off the list each weekday.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

We’re All Cats on a Hot Stove

Waiting for a correction in the stock market? It may have already happened.

If a cat sits on a hot stove, that cat won’t sit on a hot stove again. That cat won’t sit on a cold stove either. That cat just don’t like stoves.

mark twain

It’s hard to believe, but the COVID market crash ended 16 months ago.

It was truly a black swan event. Something that came out of nowhere and was unlike anything the global financial markets have seen in over 100 years.

One of the most common questions we receive is, “When is the next crash going to occur?”

This is a good question, and a very logical one. And one we think about quite often.

After all, we are seeing a rise in the Delta variant, many cities are re-instituting mask policies, and there is discussion of additional lock-downs. Sounds like February and March 2020, right?

On top of that, we have the random 1,000-point decline that happened on July 19th. Read our comments in our article “Are the Dog Days of Summer Over?“

So there are valid reasons to be expecting a sharp market decline.

But we have been receiving this question for well over a year now.

In the past year, there has been a great deal of hesitation to put cash to work in the stock market. Granted, some people were very quick to put cash to work, but most were very hesitant. And many remain so to this day.

Why?

To fully answer both the question “Why?”, and the question of whether we should expect another market crash soon, we need to understand the human behavior factors at play.

We’re All Cats That Sat on a Hot Stove

As humans, we don’t arrive at skepticism by accident.

In fact, being skeptical is an extremely valuable survival tool. Especially when we see conditions that were similar to past experiences that caused us pain or harm.

The are three basic components of skepticism:

- You perform an action.

- You experience pain.

- You learn to avoid the conditions that caused the pain.

It isn’t rocket science. In fact, we can probably just file this alongside the long list of other things we’ve said that won’t win us a Nobel prize.

In the quote that we referenced at the beginning of this report, Mark Twain presents the ultimate completion of this three-step cycle:

- A cat sits on a stove.

- The cat burns his you-know-what.

- The cat never sits on a stove again, regardless of whether it is hot or cold. Because every stove now looks like a hot stove to the cat.

Pretty simple, right?

Sort of.

Most problems in life arise when we forget to do Step 3: Learn from past experiences.

We have all experienced situations that may have caused us pain that we ended up right back in for no good reason.

Substance addiction, bad relationships, a bad job…there are all sorts of examples of people forgetting about Step 3.

Many times we’re cats who sit right back on top of that stove. And many times we are once again burned.

But what happens if learning from past experiences is the REASON we are harmed in the future?

What if we perform Step 3 beautifully, learn to avoid the situation that caused harm, only to then be harmed MORE by the fact that we avoided the situation that previously caused us pain?

This is what happens in financial markets.

When you lose money in the stock market, you have to go back on the same exact stove that burned you if you want to get back in.

This is where the complexity starts to set in.

In markets, you have to think about Step 3 differently.

The lesson learned cannot be one of complete avoidance.

You must have the cognitive ability to reshape HOW you learn lessons about what got you in trouble in the first place.

After losing money in a big market decline, most of us think that the lesson should be to NOT get back onto the market stove. After all, it looks pretty hot, right? Delta variant, super high valuations, a massive rally from last March and an out-of-control Fed all make us think the temperature on the stove is pretty darn hot.

But just because these things are happening doesn’t mean you should avoid it altogether.

Don’t Avoid the Stove, Just Start to Use a Thermometer

Instead of avoidance, you must begin to use tools that can assess both the current temperature of the stove (markets), as well as the direction and rate of temperature change of that stove.

It is a rational response to avoid the stock market after getting walloped by it. In fact, it is the exact response that would help you avoid that pain in the future.

Many investors go through a big decline and turn into real estate investors. Or private equity investors. And that’s okay.

Markets are not for everyone.

But don’t believe that getting burned on stove means that there is something inherently wrong with stoves.

There is an opportunity cost to avoiding the stove.

The public financial markets provide access to fantastic investment opportunities with a tremendously high degree of liquidity. The primary benefit of liquidity, or the ability to get out of your investment quickly at little to no cost, is that you don’t have to be right all the time. You can change your mind and you can easily get out of things that aren’t working.

You simply need to start using tools that allow you to assess the temperature of the market.

At Ironbridge, we use a wide variety of tools. We won’t get into the specifics, but we use momentum analysis, trend analysis, RSI, MACD, DeMark Signals, and many other data points that help direct our decision-making. We have then developed sets of rules that drive our actions.

The whole point is that it’s important to have some gauge of the temperature of that burner, and not not simply guess when we jump onto it.

So Is the Stove Hot or Cold Right Now?

Okay, enough of the long analogy about stoves. Let’s get to the market analysis.

Bottom line, while the S&P 500 has not seen a correction since last November, we have already seen a correction in many assets.

Let’s look at the following charts to show what we’re talking about:

- Russell 2000 (Small Caps)

- China Stocks

- Emerging Market Stocks

- Big Tech Names

- S&P 500 Sectors

- S&P 500 Index itself

Before we start, a brief note on stock corrections.

Corrections can take two forms. They can happen via TIME, or via PRICE.

A price correction is what we usually think of when we think about a market pullback. Stock prices were going up, then they fall anywhere from 5% to 30%. Then resume their move higher.

But markets can correct in TIME as well. This simply means that they go through an extended, multi-month period with little price movement up or down.

Both time and price corrections serve the same purpose: remove excesses from the markets and get the ratio of buyers and sellers more in balance.

Okay, on to the charts.

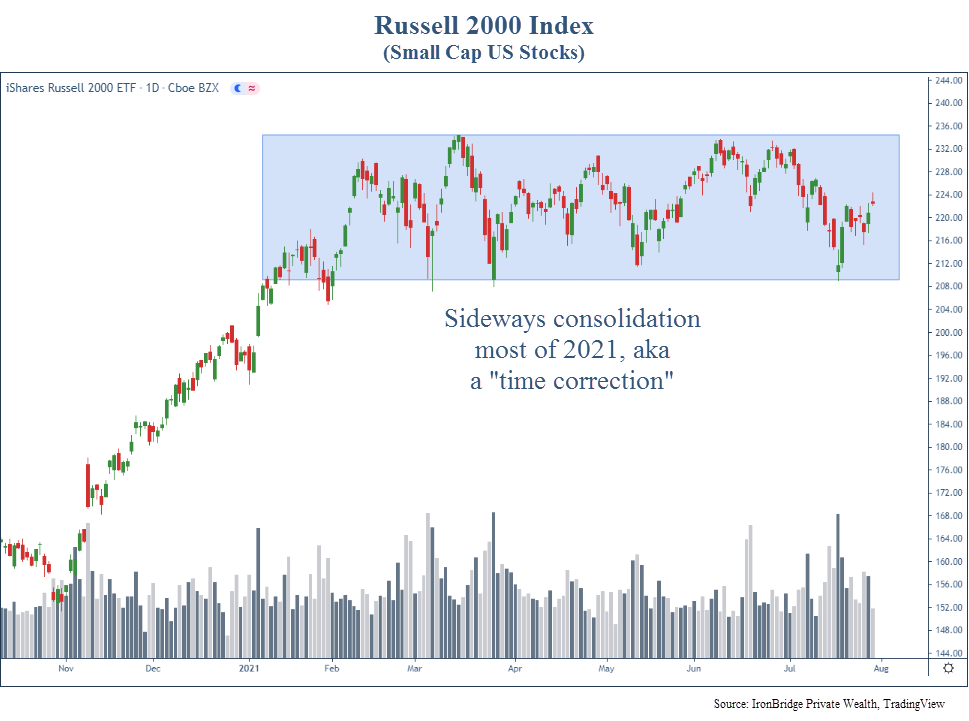

Russell 2000 (Small Caps)

First, let’s look at the Russell 2000. After a strong surge following the Presidential election, small caps have been little changed since February/March.

The blue box in the chart above is a classic correction in TIME. Small caps have been choppy with no direction for six months now. These patterns tend to resolve themselves higher, so we should expect that as the base case scenario.

However, a break below 208 in the chart above would be a more ominous signal. This could lead to selling pressure expanding across the market, and not just be isolated to small caps.

International Stocks

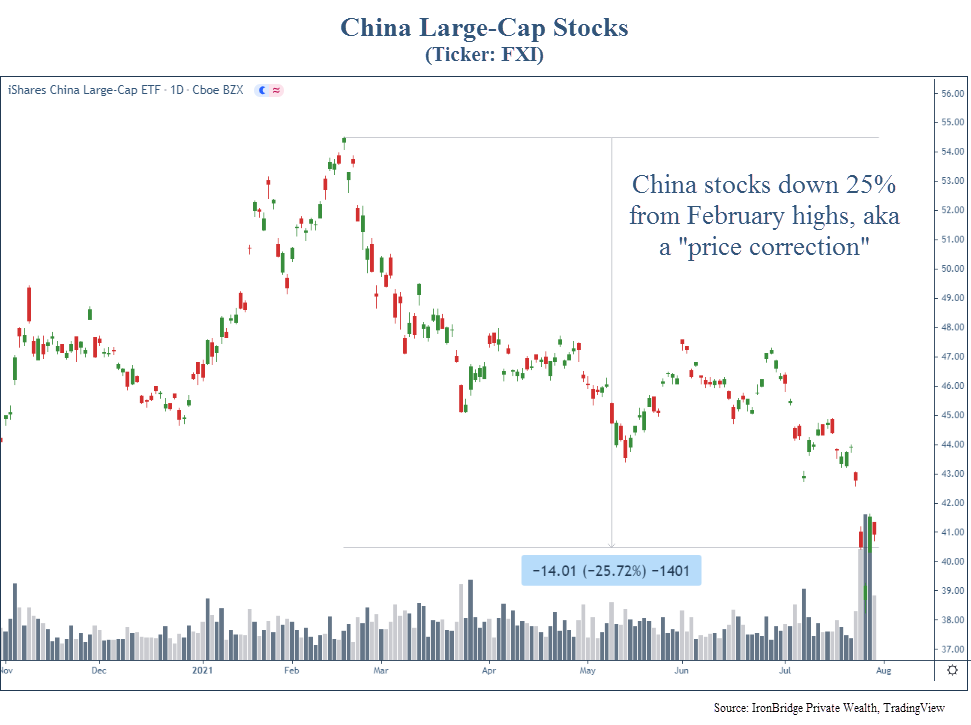

Next, let’s look at China and other international stocks.

The next chart is that of China Large Cap Stocks, using the ticker FXI.

This is a classic correction in PRICE. Stocks are down 25% since February. There is little doubt the direction of this trend.

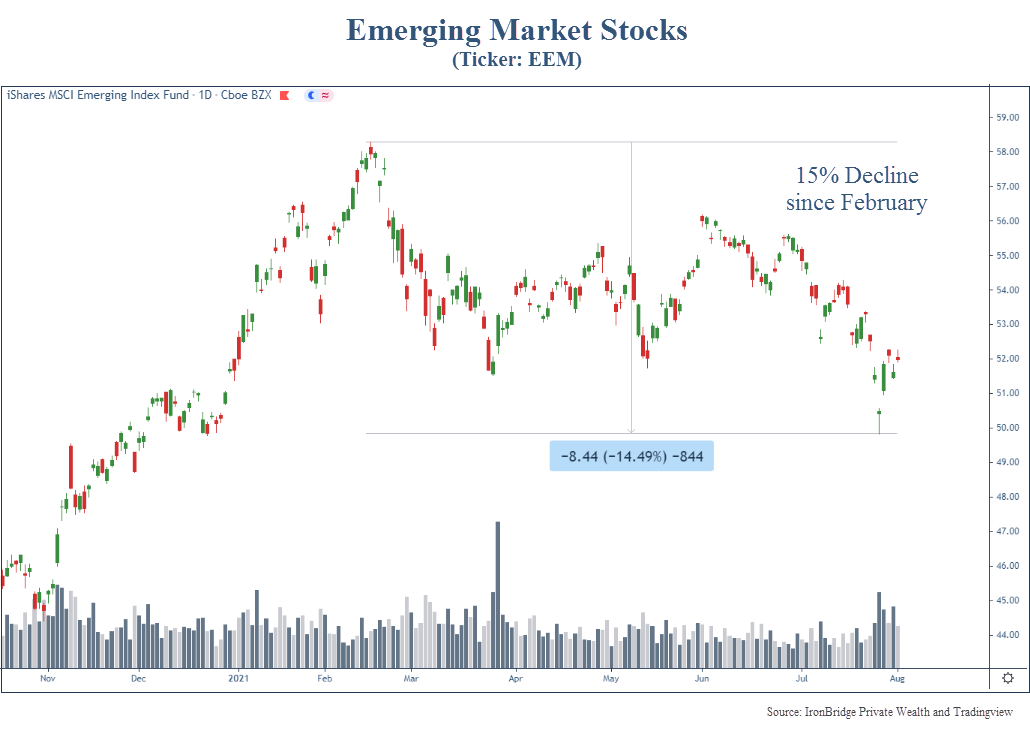

The same is true of other, more broad international stock indices.

Emerging market stocks are down over 15%, as shown in the next chart. This is no real surprise since China is the largest component. But it is another example of a major global equity market component that is experiencing a correction right now.

International stocks have been weak. There is no question about that.

U.S. Stocks

What about some of the major U.S. stocks?

Well, here is when we start to see what is really happening in U.S. stocks right now.

The next chart shows four of the largest U.S. stocks: Amazon, Apple, Microsoft and Netflix.

These charts show us that each of these stocks went through some sort of TIME correction in the past year.

- On the top left of the chart is Amazon (AMZN). It was in a sideways move for almost a year. It broke higher, but fell back into it’s chop zone last Friday after a 7% decline following earnings. This is called a “false breakout”. Meaning it may have longer to go before it breaks out of its sideways correction.

- Apple (AAPL), on the top right, shows a classic break higher from a sideways correction. It also spent over a year in a TIME correction before resolving higher.

- Microsoft (MSFT), on the bottom left, was in a TIME correction for the second half of last year. It has steadily been moving higher since the start of the year.

- Finally, Netflix (NFLX) is shown on the bottom right. This was a darling of the COVID period, and remains in a TIME correction since this time last year.

Each of these stocks experienced a correction. And these are major components of the S&P 500.

The fact that these stocks are breaking higher suggests we should have a bullish tilt to our thinking.

S&P 500 Sectors

Looking some of the sectors in the S&P 500, we see a similar picture.

The next chart looks at the Energy, Industrials, Tech, Financials and Consumer Discretionary sectors. We could have chosen more, but the chart gets way too busy.

Each of these sectors have all seen some sort of correction in the past year. Most have been correcting in TIME.

Energy has been the biggest winner since the election. There is an excellent lesson here. The pundits on CNBC and elsewhere all predicted a Biden presidency would harm energy companies. That would make sense logically. But the market responded in exactly the opposite way. The lesson? Using the financial media for investment decisions is not a sound strategy.

This sideways movement of the major S&P sectors suggests that corrections are actually happening under the surface of the market.

But what about the overall market itself?

S&P 500 Index

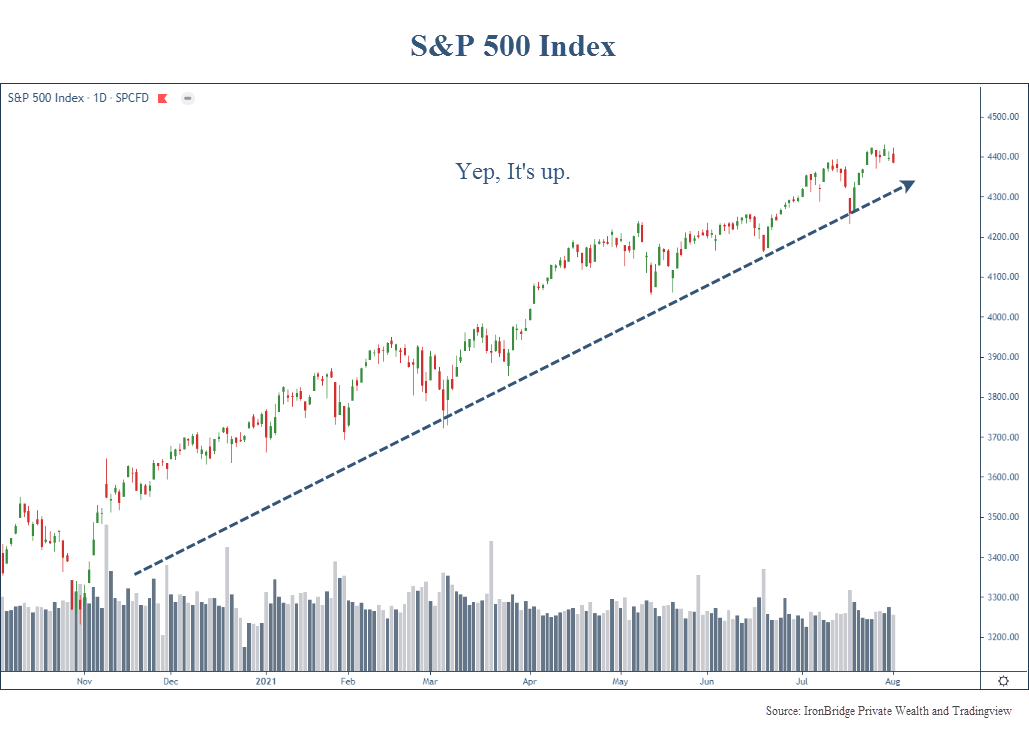

But here’s the strange thing: Despite corrections happening in both the major stocks and major sectors within the index, the S&P 500 Index itself has been very strong.

Despite the underlying TIME corrections happening in various sectors, and despite the obvious PRICE correction in international markets, the S&P 500 is up. In a very, boring, beautiful pattern higher.

So What Does All of This Mean?

It means that if you’re expecting a stock correction, it may have already happened.

As strange as this sounds, the underlying components in the markets have all mostly corrected already. Without an overall market correction.

Chalk this up as a win for indexers.

This is also why at IronBridge we have both active and passive strategies in place.

In fact, we have had the highest exposure to the S&P Index in our four-year history. We could only go about 5% higher in our portfolio weighting to the S&P 500 Index based on our rules. At the high point, clients had exposure of anywhere from 25-35% of their portfolios, depending on the risk level.

While the S&P has been boring, it’s more interesting to look at the small caps and international stocks.

Earlier this year, our clients had exposure to both of these areas. And both were stopped out at relatively small losses.

For small caps, that wasn’t such a big deal. Prices are similar to where they were when we exited.

But for international stocks, they are down 15-20% lower than where we exited.

Such is the nature of risk management.

We don’t know when things will reverse higher, chop sideways, or continue lower. Guess what, no one else does either.

But was has been interesting about this year is that there has been both volatility and no volatility at the same time. The stove is both hot and cold.

So it would be completely logical to expect the S&P to experience some sort of correction, either in PRICE or TIME.

But the underlying components suggest that we shouldn’t bank on it either.

There is a chance we have already seen the correction via the underlying components and the selloff in other areas.

If this is the case, the second half of this year should be strong. And will likely extend into next year.

If the S&P 500 does start to experience a correction, the likelihood is that it is relatively mild and most likely happens via a TIME correction.

In the meantime, look for opportunities to put cash to work, and stick with a disciplined risk management process.

Invest wisely!

Building Your Life Team

A time-tested piece of career advice is to find a mentor.

But as the world gets more complex, simply having a good career mentor isn’t enough.

You need a team. In today’s reality of multiple jobs, the ability and ease of changing your career path and the sheer number of choices we face every day, one mentor isn’t really going to cut it. The new approach is to build a team that can help you create an intentional life.

Your relationships, your community, your work…all your choices should help you build towards the life you want – while ensuring you can stay true to yourself along the way.

There’s no blueprint or roadmap to help us know if we’re making the right decisions or not.

But there is one thing you can do to help make it easier: build a ‘life team’.

What Is a Life Team and Why Would You Need One?

A life team is a hand-selected group of people that you believe can bring value to your life. This is not like on the playground at recess where you pick the most athletic team member.

Your life team is made up of people with a myriad of skills, experiences and strengths that can provide valuable, timely advice and help you navigate through the challenges and complexities of life.

It’s easy to think that as we go through life we must fend for ourselves; however this is far from the truth. Being able to learn from others and bounce ideas off each other can be beneficial to both parties. And having trusted professional relationships can help in many aspects of life.

They can act as a sounding board for tough decisions. Be there to help with decision-making when at a crossroads. And provide emotional support when the going gets tough.

We’ve broken down the big areas where you may want to find counsel and support in different disciplines – but of course, all of these can work in multiple situations.

Building Your Financial Foundation

One aspect of your life team that may already be established is your financial team. This consists of professionals that can help navigate the financial side of life and typically includes roles such as a wealth advisor, a CPA, and an attorney.

Since everyone has to file taxes, a CPA is usually one of the first relationships that gets established. However, CPAs and accountants usually do more than just taxes and can play a critical role when it comes to helping to build your wealth.

And just like an accountant does more than just taxes, wealth advisors typically do more than just investments. Having a trusted wealth advisor in your corner may turn out to be one of the best investments you make. Primarily because they help steer the ship in your financial life. From helping manage financial risk to growing your net worth to helping uncover and clarify your goals, a financial advisor is there with you through it all.

And when it comes to the legal aspect of finances, a trusted attorney is another professional relationship that can bring value. One of the biggest aspects of your financial life that an attorney can help with is estate planning. You’ll want to get this started early, and keep them updated about your situation over time, so they can provide better solutions as things change.

Ideally, these three professionals will work in tandem to provide you with confidence and clarity in both your professional and your financial life.

Finding Your Guides Through Life

Most of us spend most of our time on a few things – our family, our hobbies and passions, and our career. When it comes to our careers, it’s easy to begin feeling stuck or complacent. That’s where career and life mentors can play a vital role.

The typical role that a life coach plays is helping individuals feel more fulfilled by clarifying their goals, identifying what’s holding them back, and then coming up with strategies to help them move forward. If you’ve felt stuck in life or in your career, a life coach may be the unlock to success and happiness.

Mentors are still valuable – you just may need more than one. With a career mentor, it’s wise to seek out someone who’s a few years ahead of you as well as someone who’s a couple decades ahead of you. The reason is because these relationships can help build perspectives that you wouldn’t have. And through these conversations, you can create a history that speeds up your own learning curve so you can effectively advance and progress through your career.

A good mentoring relationship is just that – a relationship. It should be valuable to both people.

Staying Centered Through It All

As we all know, life comes at us fast. We’re always solving the next problem while trying to keep up with our current way of life and finding time to work on careers while spending time with family, while following your own passions and interests. It’s tough to find that fleeting equilibrium that we call work-life balance.

A common route that people take when trying to find balance in their life is picking up new or forgotten hobbies. This may be something you enjoyed as a kid that got pushed to the side as life picked up speed, or a passion that you’ve never had the time to explore. Having a hobby or activity that can help take your mind off the day to day stresses of life is an effective way to not only stay centered, but to also live a more fulfilled life.

The rise of our digital lives, and in particular social media, is often cited as one of the negatives of modern society – but there is a big benefit, if you avail yourself of it. The proliferation of apps, blogs, and influencers who focus on wellness makes it incredibly easy to incorporate these elements into your life. The level of comfort we all have now with videoconferencing has added yet another element.

Creating a meditation practice, developing a yoga or other spiritual-based exercise routine you can incorporate into your mornings, even joining a like-minded community that works towards change – these can all add a necessary element of discipline, health and clear-mindedness that can be hard to access as we go through our daily lives.

The Takeaway

Through intentional relationship building, you can begin to form a team of people around you that can provide valuable advice and necessary feedback.

When seeking out a life team, it’s important that you first understand your own weaknesses so you can determine the most impactful relationships to build.

To get the most out of your life team, make sure you stay in regular contact and share updates, accomplishments, and challenges because this will make them feel like they’re a part of your story and your mission which will only increase the value of the relationship for everyone.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

Are the Dog Days of Summer Over?

A calm summer for the markets was interrupted today with a large selloff. Is this just a blip, or is it the start of a bigger decline?

What happened:

- Dow Jones Industrial Index closed down 725 points, or 2.09%

- S&P 500 was down 68 points or 1.59%

- The media blamed COVID fears, but it looks more technical in nature

- VIX Index rose nearly 40% at one point during the day

- Bonds had their best day of the year, with long-term US Treasury prices up over 2%

Near-Term Market Assessment:

- Numerous warning signs have been happening over the past three months:

- Lumber prices have fallen 68% from their highs.

- 10-Year Treasury Yields have dropped from 1.76% in March to 1.19% today.

- Fewer stocks have been participating in the slow drift higher since mid-February. Today, more than 50% of the stocks in the S&P 500 are below their 50-day moving average (more on this below). That number has been steadily rising since April.

- It is too early to tell if this selloff will continue. Bull markets tend to have short, sharp declines like this.

- The S&P 500 Index is only 3% off its all-time highs. So the fear seems somewhat unwarranted at this point.

Portfolio Implications:

- We have been systematically raising our stop-losses over the past few months.

- We sold two positions today, one stock ETF and a high-yield bond ETF. Both moved to cash equivalent ETFs.

- We may get further sell signals this week. If we do raise cash this week, it may not remain in cash very long if the market decides to resume its move higher.

- We do not know when a short-term decline will turn into a long-term decline. That’s why we have rules and don’t try to guess. This kind of environment has the potential for a “whipsaw”, where we move from invested to cash and back to being invested. This is definitely not the favorite part of our process, but it is a natural consequence of having disciplined rules and not just winging it.

Market Discussion

Markets were down over 2% today. The primary (and easy) explanation is COVID. Every state in the US is showing a rise in cases. Los Angeles reinstated mask requirements this past weekend (even for those fully vaccinated). Other parts of California and possibly New York City may follow suit with mask requirements.

Naturally, any volatility in the markets is blamed on the most recent “thing”. It’s natural to assume that the rise in cases we are seeing now would result in a market environment like we saw in early 2020. We’re human and that’s what we do…extrapolate past events and assume they will happen again.

But the reality is that there were plenty of factors to explain the move lower today.

And they are mainly technical in nature.

First, market breadth has been very narrow the past few months.

This simply means that fewer and fewer stocks have been in uptrends, despite markets drifting higher. In fact, many stocks have been in downtrends since April.

The chart below shows the percentage of the S&P 500 Index that has been above its 50-day moving average (50dMA).

The 50dMA is simply the average price of a stock over the last 50 trading days. A stock above that level is generally considering to be in a rising trend (or a bull market). A stock that falls below that level is considered to be in a declining market.

What the chart above shows us is that while the market has been drifting higher, over 50% of the stocks in the index were in bear markets in June. This is referred to as “breadth”.

This indicator is similar to a game of jenga. When there are many blocks supporting the tower at the start of the game, the tower is strong and sturdy.

But as the game goes on, there are fewer blocks supporting the ever increasing height of the jenga tower.

This is happening in the stock market. When there are a lot of stocks supporting the index, it is more sturdy. In April, over 90% of the stocks in the S&P 500 Index were above their respective 50dMA. But as more and more stocks begin to reverse trend and fall, the index get wobbly.

This is very similar to mid-2018. We wrote about breadth in our “Soldiers are AWOL” report. After a weakening breadth environment in mid-2018, the market corrected by 20% in Q4 of that year.

The big tech stocks have been doing the heavy lifting in the past three months. The same exact thing happened in 2018.

The next reason is simply that the market is overdue for a correction.

So while COVID is to blame, the fact remains that we are due for a pause following the massive rally from the COVID lows last year. The market has had very little pauses, and is well overdue for a correction.

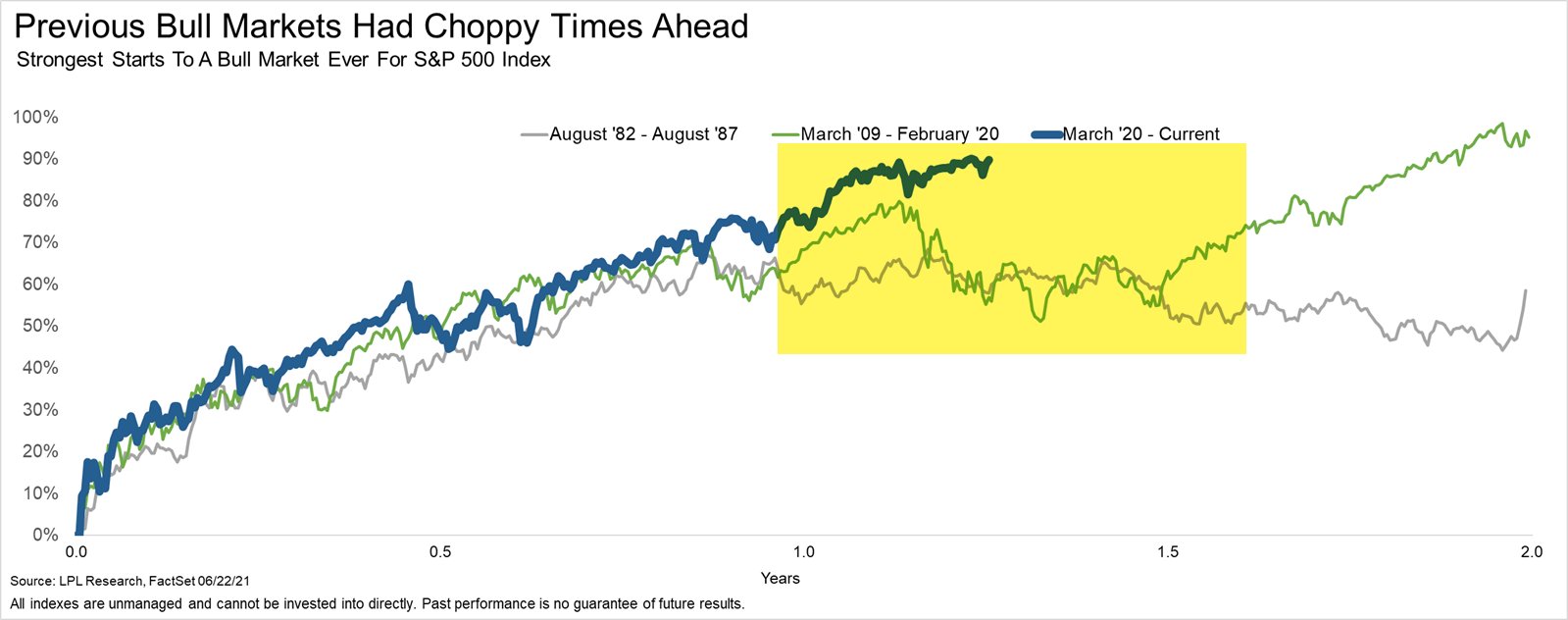

We shared the next chart in our last email newsletter, but it’s worth sharing again.

This shows the market rallies from previous major bear market bottoms. Three environments are shown here (1982, 2009 and 2021).

This chart suggests we are due for a natural pause given the strength of the move from March 2020’s lows.

So while the news is blaming COVID, the reason for today’s selloff seems to be much more technical in nature than simply worry about the delta strand.

The next few days will provide tremendous insight into what may happen over the coming weeks and months.

We had two sell signals today, selling one stock ETF and a high-yield bond ETF.

There is a chance we get many more sell signals this week.

However, no one knows if this is just a blip or if it is the start of something bigger.

Given the positive trends in the economy, continued massive support from the Fed, and the very technical nature of the market selloff today, we should assume that the bull market is still in tact, but due for a pause.

Risk management is a priority for us and our clients. Therefore, we will not wait to see what happens. We will act on our signals, and adjust course as necessary.

That could mean increased cash, but it could also mean that cash on the sidelines today gets put back to work very shortly.

Either way, the dogs days of summer could indeed be over for the stock market, even if it simply means a temporary pause in the bull market.

Please do not hesitate to reach out with any questions or concerns you have.

Invest wisely!

Managing an Inheritance

Inheriting wealth can be a burden and a blessing. Even if you have an inclination that a family member may remember you in their last will and testament, there are many facets to the process of inheritance that you may not have considered. Here are some things you may want to keep in mind if it comes to pass.

Keep in mind this article is for informational purposes only and is not a replacement for real-life advice, so consider speaking with a legal or tax professional before making any decisions with an inheritance.

Take your time. If someone cared about you enough to leave you an inheritance, then you may need time to grieve and cope with their loss. This is important, and many of the more major decisions about your inheritance can likely wait. You may be able to make more informed decisions once some time has passed.

Don’t go it alone. There are so many laws, choices, and potential pitfalls – the knowledge an experienced professional can provide on this subject may prove critical.

Think of your own family. When an inheritance is received, it may alter the course of your own financial strategy. Be sure to take that into consideration.

The taxman may visit. If you’ve inherited an IRA, it is important to consider the tax implications. Under the SECURE Act, distributions to non-spouse beneficiaries are generally required to be distributed by the end of the 10th calendar year following the year of the account owner’s death.

It’s also important to highlight that the new rule does not require the non-spouse beneficiary to take withdrawals during the 10-year period. But all the money must be withdrawn by the end of the 10th calendar year following the inheritance. A surviving spouse of the IRA owner, disabled or chronically ill individuals, individuals who are not more than 10 years younger than the IRA owner, and children of the IRA owner who have not reached the age of majority may have other minimum distribution requirements.

Stay informed. The estate laws have seen many changes over the years, so what you thought you knew about them may no longer be correct.

Remember to do what’s appropriate for your situation. While it’s natural for emotion to play a part and you may wish to leave your inheritance as it is out of respect for your relative, what happens if the inheritance isn’t appropriate for your financial situation? A financial professional can help determine if the inheritance fits with your overall goals, time horizon, and risk tolerance.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2021 FMG Suite.